Enabling

Deliver world class digital financial solutions, that enable seamless experiences for:

- digital onboarding

- QR transactions

- identity validation

- business banking services

- conversational banking

- fraud prevention

- mobile banking

- SaaS solutions

- cross selling opportunities

- digital onboarding

- online loan applications

- conversational banking

- business banking

- improve debt collection rates

- key banking features

Our channels

-

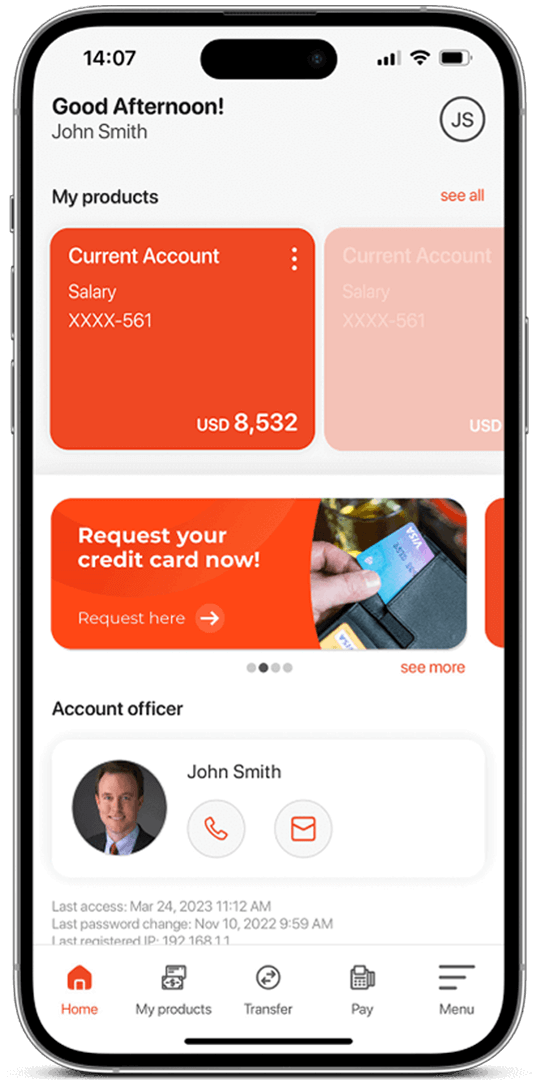

Internet Banking

Empower clients' finances with our dynamic duo—a modern app featuring innovative features, customizable design, and comprehensive functionalities. Elevate the way you bank today.

-

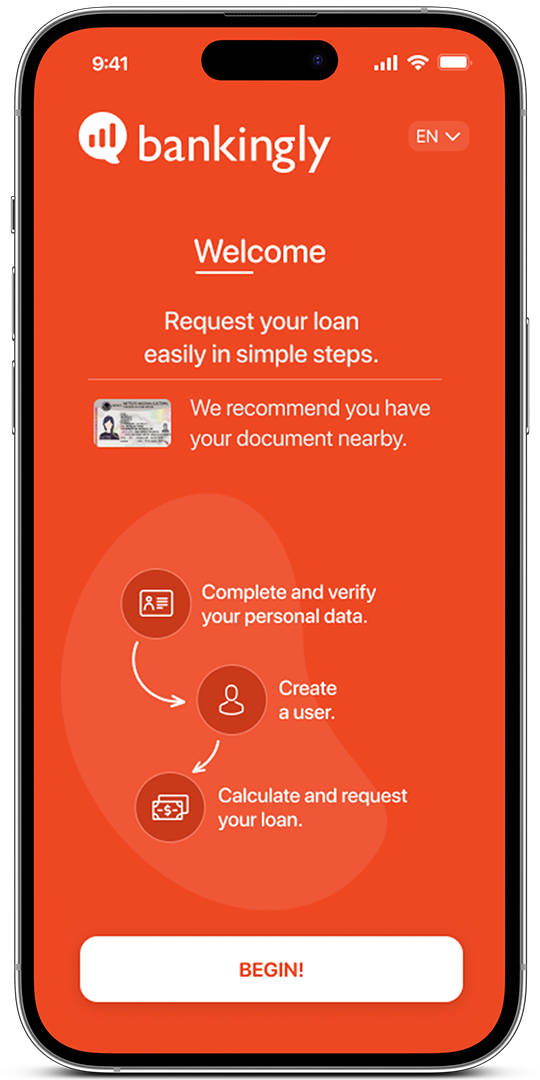

Digital Onboarding

Streamline customer interactions. Effortlessly apply for new financial products with enhanced efficiency and security. Validate user information seamlessly through advanced biometric verification.

-

Conversational Banking

Improve engagement and customer satisfaction through more assertive, personalized and real-time communication on social networks.

Internet Banking

Empower clients' finances with our dynamic duo—a modern app featuring innovative features, customizable design, and comprehensive functionalities. Elevate the way you bank today.

Digital Onboarding

Streamline customer interactions. Effortlessly apply for new financial products with enhanced efficiency and security. Validate user information seamlessly through advanced biometric verification.

Conversational Banking

Improve engagement and customer satisfaction through more assertive, personalized and real-time communication on social networks.

Clients Testimonials

Learn how our digital solutions have streamlined our clients' banking processes. Understand why Bankingly plays a pivotal role in their digital transformation journey.

+100

clients

+3.5M

people reached

+60

collaborators

Where

we are +20

countries

we are +20